These formulas aren’t just numbers—they’re decision-making tools. Understanding what drives each one helps you actually improve your finances, not just calculate them.

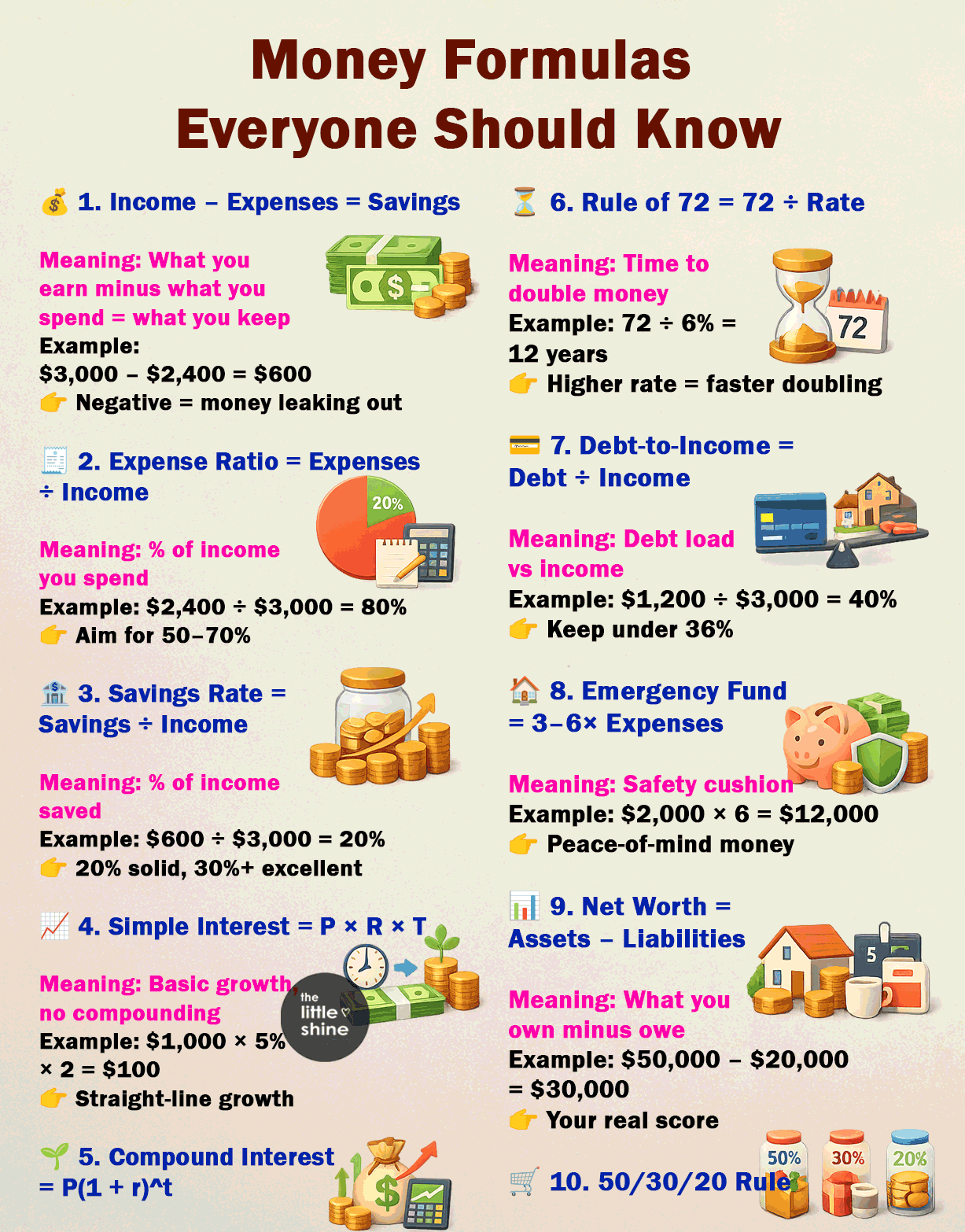

1. Income – Expenses = Savings

What it means:

This is your financial baseline. It shows whether your lifestyle is sustainable.

Example:

$3,000 – $2,400 = $600 saved

Extra insight:

- If savings = $0, you’re financially stagnant.

- If negative, you’re relying on debt or dipping into reserves.

- Improving this isn’t only about earning more—it’s often about controlling fixed expenses (rent, EMIs, subscriptions).

2. Expense Ratio = Expenses ÷ Income

What it means:

Shows how efficiently you use your income.

Example:

$2,400 ÷ $3,000 = 80%

Extra insight:

- High ratios reduce flexibility and increase stress.

- Fixed costs (housing, loans) usually drive this number up.

- Aim to lower “non-essential leakage” like impulse spending, subscriptions, and frequent dining out.

3. Savings Rate = Savings ÷ Income

What it means:

Your most important wealth-building metric.

Example:

$600 ÷ $3,000 = 20%

Extra insight:

- This directly determines how fast you can build wealth.

- Increasing your savings rate by even 5–10% has a massive long-term impact.

- Automating savings (auto-transfer to investments) makes consistency easier.

4. Simple Interest = P × R × T

What it means:

Interest earned only on the principal amount.

Example:

$1,000 × 5% × 2 = $100

Extra insight:

- Common in short-term loans or basic financial products.

- It does not benefit from time the way compounding does.

- Good for understanding basic borrowing costs, but not ideal for long-term investing.

5. Compound Interest = P(1 + r)^t

What it means:

Growth on both principal and accumulated interest.

Example:

$1,000 at 5% for 2 years = $1,102.50

Extra insight:

- Time is the biggest factor here—not just rate.

- Starting early beats investing larger amounts later.

- Missing years of compounding can significantly reduce long-term wealth.

6. Rule of 72 = 72 ÷ Rate

What it means:

Quick mental math to estimate doubling time. In the Rule of 72, the “rate” means the annual interest rate (or return rate) expressed as a percentage.

Example:

72 ÷ 6% = 12 years

Extra insight:

- Useful for comparing investment options quickly.

- Also applies to inflation—money loses value over time at a similar rate.

- Small increases in return can dramatically reduce doubling time.

7. Debt-to-Income Ratio = Debt ÷ Income

What it means:

Indicates how much of your income is tied up in debt payments.

Example:

$1,200 ÷ $3,000 = 40%

Extra insight:

- Lenders use this to assess your risk.

- High DTI reduces your ability to save or invest.

- Focus on reducing high-interest debt first (like credit cards).

8. Emergency Fund = 3–6 × Monthly Expenses

What it means:

A buffer for unexpected situations.

Example:

$2,000 × 6 = $12,000

Extra insight:

- If income is unstable (freelancing/business), aim closer to 6 months or more.

- Keep this money liquid (savings account, not locked investments).

- This prevents you from going into debt during emergencies.

9. Net Worth = Assets – Liabilities

What it means:

Your overall financial health.

Example:

$50,000 – $20,000 = $30,000

Extra insight:

- Assets include cash, investments, property.

- Liabilities include loans, credit cards, mortgages.

- Track this every 6–12 months to measure real progress—not just income.

10. 50/30/20 Rule

What it means:

A structured way to allocate income.

Example (on $3,000):

- Needs: $1,500

- Wants: $900

- Savings: $600

Extra insight:

- This is a guideline, not a strict rule.

- In high-cost cities, “needs” may exceed 50%—adjust accordingly.

- If you want faster wealth growth, shift toward 50/20/30 or even 50/10/40 (higher savings).

Final Takeaway

These formulas work best when used together—not in isolation. Tracking them monthly gives you a clear picture of where your money is going and how to improve it.